Published by Sherry Cooper

Weak Canadian job growth in March and rising unemployment is the first harbinger of a trade-war induced economic slowdown.

Weak Canadian Job Creation Is The First Fallout From The Trade War

Today’s Labour Force Survey for March was weaker than expected. Employment decreased by 33,000 (-0.2%) in March, the first decrease since January 2022. The decline in March followed little change in February and three consecutive months of growth in November, December and January, totalling 211,000 (+1.0%).

The employment rate—the proportion of the population aged 15 and older—fell 0.2 percentage points to 60.9% in March. This partially offsets an increase of 0.3 percentage points observed from October 2024 to January 2025.

Private sector employment fell by 48,000 (-0.3 %) in March, following little change in February and a cumulative increase of 97,000 (+0.7%) from November 2024 to January 2025. On a year-over-year basis, the number of employees in the private sector was up by 175,000 (+1.3%).

Public sector employment was little changed for a third consecutive month in March, up 92,000 (+2.1%) compared with a year earlier. Self-employment was also little changed in March, up 81,000 (+3.0%) on a year-over-year basis. Economists expected the trade war to weigh on the Canadian labour market in March. Market participants expected zero employment gains as steel & aluminum tariffs hit jobs in the sector. While we haven’t seen broad-based layoffs yet, automaker Stellantis NV temporarily halted production at assembly plants in Windsor, ON and Mexico, laying off 3,200 people in Canada, 2,600 in Mexico and 900 at six U.S. factories. The pressure from those and broader non-USMCA-compliant tariffs was expected to drive stagnant job growth in the month. At 6.7%, the jobless rate met expectations, still two ticks shy of November’s cycle high.

Employment could experience a further downside over the coming months, depending on how the tariff backdrop evolves. Average hours worked could see an even bigger hit as work-sharing programs come into effect due to pressure on manufacturing production.

The unemployment rate rose 0.1 percentage points to 6.7% in March, the first increase since November 2024. It had trended up from 5.0% in March 2023 to a recent high of 6.9% in November 2024 before falling by 0.3 percentage points from November 2024 to January 2025 in the context of robust employment growth at the end of 2024 and in early 2025.

Since March 2024, the unemployment rate has remained above its pre-COVID-19 pandemic average of 6.0% (from 2017 to 2019).

In total, 1.5 million people were unemployed in March, up 36,000 (+2.5%) in the month and up 167,000 (+12.4%) year over year.

Among those unemployed in February, 14.7% became employed in March. This was lower than the corresponding proportion in March 2024 (18.6%) (not seasonally adjusted). Long-term unemployment has also risen; the proportion of unemployed people searching for work for 27 weeks or more stood at 23.7% in March 2025, up from 18.3% in March 2024.

Total hours worked rose 0.4% in March, following a decline of 1.3% in February. On a year-over-year basis, total hours worked were up 1.2%.

Average hourly wages among employees were up 3.6% (+$1.24 to $36.05) year over year in March, following growth of 3.8% in February (not seasonally adjusted).

Fewer people are employed in wholesale and retail trade, information, culture, and recreation.

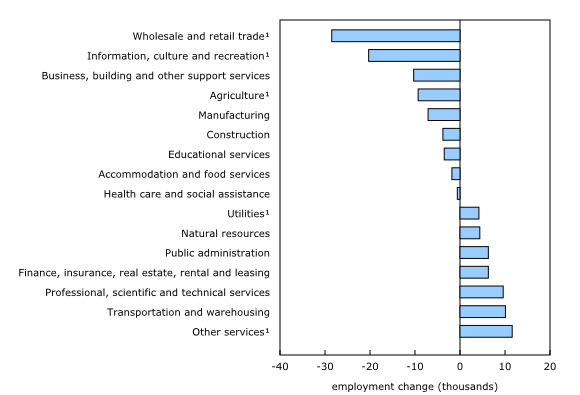

Wholesale and retail trade employment fell by 29,000 (-1.0 %) in March, partly offsetting an increase of 51,000 in February. On a year-over-year basis, the number of people working in wholesale and retail trade was little changed in March.

Chart 3

Employment declines led by wholesale and retail trade in March

{kind=link}

Following five months of little change, employment in information, culture, and recreation decreased by 20,000 (-2.4%) in March. Despite the decline, employment in this industry changed little on a year-over-year basis.

In March, employment also fell in agriculture (-9,300; -3.9%), while there were gains in “other services” (such as personal and repair services) (+12,000; +1.5%) and in utilities (+4,200; +2.8%).

Bottom Line

US employment data for March were also released this morning. In direct contrast to Canada, US job growth beat forecasts in March, and the unemployment rate edged up, pointing to a healthy labour market before the global economy gets hit by widespread tariffs.

Canada’s job market stalled in March, shedding the most jobs in over three years. The job loss was the first in eight months, with trade-exposed sectors driving some declines.

The threats and implementation of US President Donald Trump’s tariffs and Canada’s retaliating levies have weighed on the Canadian jobs market over the past two months. However, with the country dodging the latest round of so-called reciprocal tariffs this week, the Bank of Canada may have more time to weigh economic weakness against rising price pressures.

Stocks have fallen the most since March 2020–the beginning of Covid, and bonds are rallying causing market-driven interest rates to drop precipitously. The Bank of Canada meets again on April 16. The day before, Canadian inflation data for March will be released. This will be a crucial report as the central bank assesses the tug-of-war between tariff-induced inflation and unemployment. Currently, traders are betting there is only a 33% chance of a 25 bps rate cut later this month. While the BoC might take a pass this month, the coming slowdown in the Canadian economy will warrant rate cuts in June, if not sooner.