Published by Sherry Cooper

Canadian Home Sales Surge in October Led by the GVA and GTA.

The Canadian Housing Market Shows Signs of Life

Canadian home sales surged to their highest level in more than two years as the Bank of Canada cut interest rates, bringing buyers back into the market. Home sales rose 7.7% month-over-month (m/m) in October, reaching their highest level since April 2022.

Rising home sales were broadly based, with the Greater Toronto Area and British Columbia’s Lower Mainland recording double-digit increases in October. The buoyant housing demand was likely the result of the surge in new listings in recent months and the fall in mortgage rates arising from the BoC’s easing. The jumbo rate cut, however, was in the last week of October, likely having little bearing on the monthly data released by the Canadian Real Estate Association this morning. Actual monthly housing activity came in 30% stronger than year-ago levels.

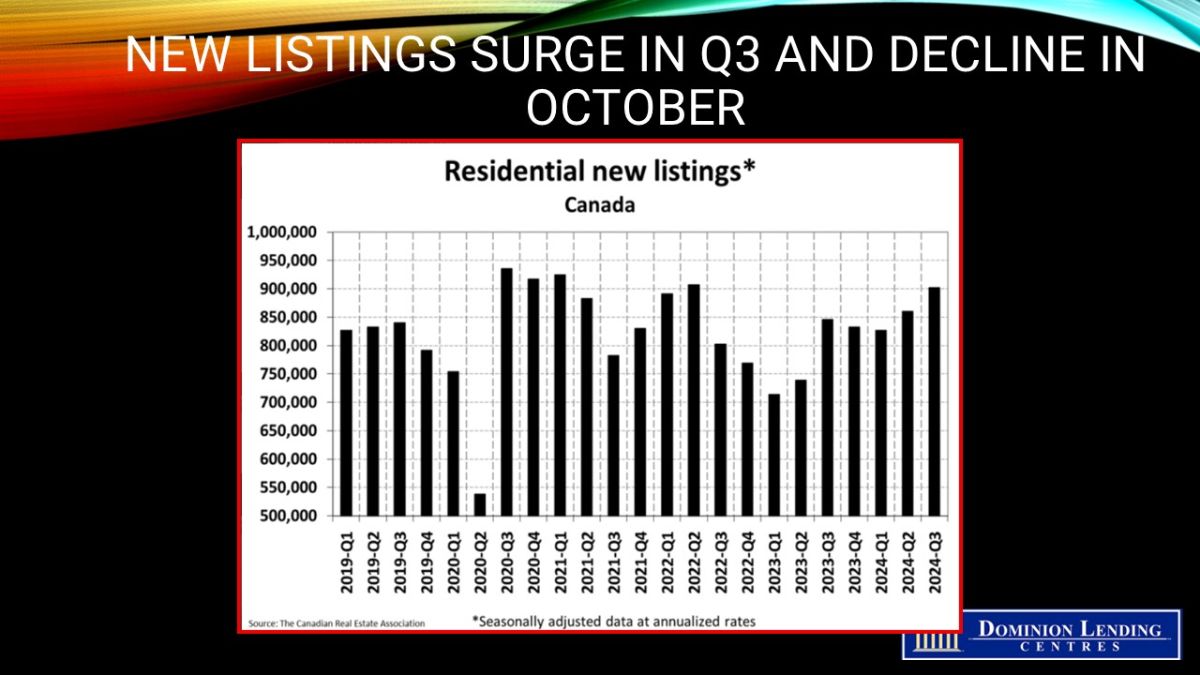

New Listings

New listings posted a 3.5% month-over-month decline in October, although that followed a 4.8% jump in September. Thus, new supply remains at some of the highest levels since mid-2022. The national pullback in October was led by a drop in new supply in the GTA.

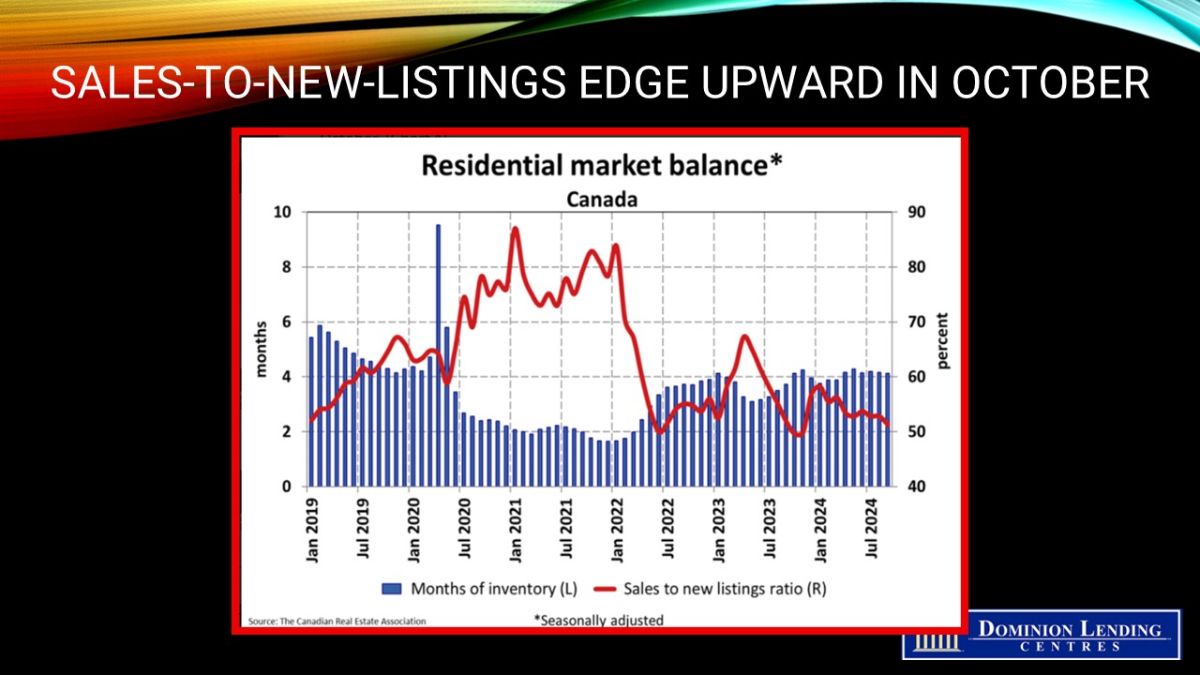

With sales rising considerably in October and new listings falling, the national sales-to-new listings ratio tightened to 58%, up from 52% in September. The long-term average for the national sales-to-new listings ratio is 55%, with a sales-to-new listings ratio between 45% and 65%, generally consistent with balanced housing market conditions.

At the end of October 2024,174,458 properties were listed for sale on all Canadian MLS® Systems, up 11.4% from a year earlier but still below historical averages for that time of year.

As of the end of October, there were 3.7 months of inventory nationwide, down from 4.1 months at the end of September and the lowest level in more than a year. The long-term average is 5.1 months of inventory, with a seller’s market below about 3.6 months and a buyer’s market above 6.5 months.

{kind=link}

{kind=link}

Home Prices

The National Composite MLS® Home Price Index (HPI) inched up 0.1% from August to September; however, small ups and downs aside, the bigger picture is that prices at the national level have remained mostly flat since the beginning of the year.

The non-seasonally adjusted National Composite MLS® HPI stood 3.3% below September 2023, a smaller decline than the 3.9% declines recorded in July and August. Given the price weakness seen towards the end of 2023, negative year-over-year comparisons will likely continue to shrink.

Bottom Line

The strength in home sales in October likely contributes to the expectation that the central bank will cut interest rates by only 25 bps when it meets again on December 11. Of course, their decision will be data-dependent; next week, we will see the October inflation data on Tuesday and retail sales on Friday. The November Labour Force Survey will be released on December 6. The unemployment rate has held steady at 6.5%, and wage inflation remains high. It would take a significant disappointment in these data to trigger another 50 bps cut.

In the meantime, bond yields continue to rise, triggered by the strong Trump victory and the fear that tax cuts and spending increases will boost government debt and deficits. While US long-term yields have risen nearly 80 basis points, Canadian 10-year yields are up less than half that amount. There is an unprecedented gap between economic activity in the US and Canada. The US dollar continues to strengthen, putting downward pressure on the loonie.

Pent-up demand for housing continues to be strong, and the combination of lower short-term interest rates and rising inventories of unsold homes will spur activity as we move into the all-important spring season. By then, the overnight rate, currently 3.75%, could be at least a full percentage point lower.