Published by Sherry Cooper

Canadian home sales rose again in November as new listings declined and prices rose.

The Canadian Housing Market Strengthens Further

Home sales activity recorded over Canadian MLS® Systems rose again in November, building on October’s surprise jump.

Sales were up 2.8% m/m in November compared to October and now stand a cumulative 18.4% above where they were in May, just before the first interest rate cut in early June. Actual (not seasonally adjusted) monthly activity was 26% above November 2023. The November increase was driven by gains in Greater Vancouver, Calgary, Greater Toronto, and Montreal and double-digit sales increases in smaller cities in Alberta and Ontario.

According to Shaun Cathcart, CREA’s Senior Economist, “Not only were sales up again but with market conditions now starting to tighten up, November also saw prices move materially higher at the national level for the first time in almost a year and a half. Normally, we might expect this market rebound to take a pause before resuming in the spring; however, the Bank of Canada’s latest 50-basis point cut together with a loosening of mortgage rules could mean a more active winter market than normal.”

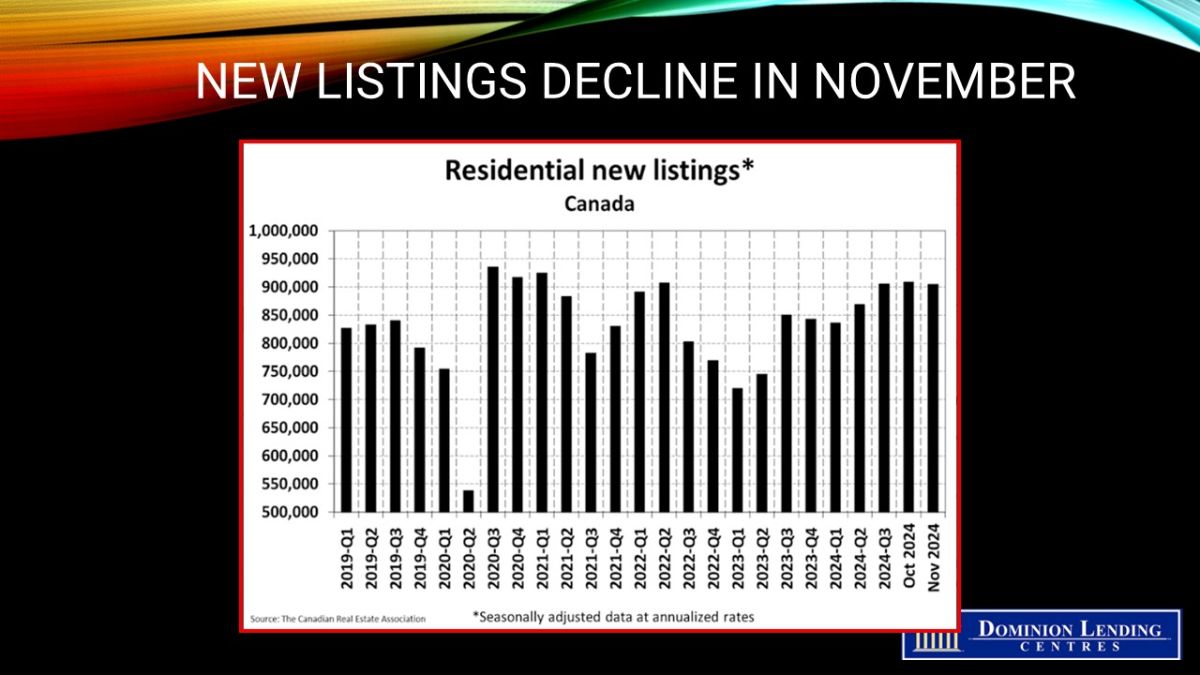

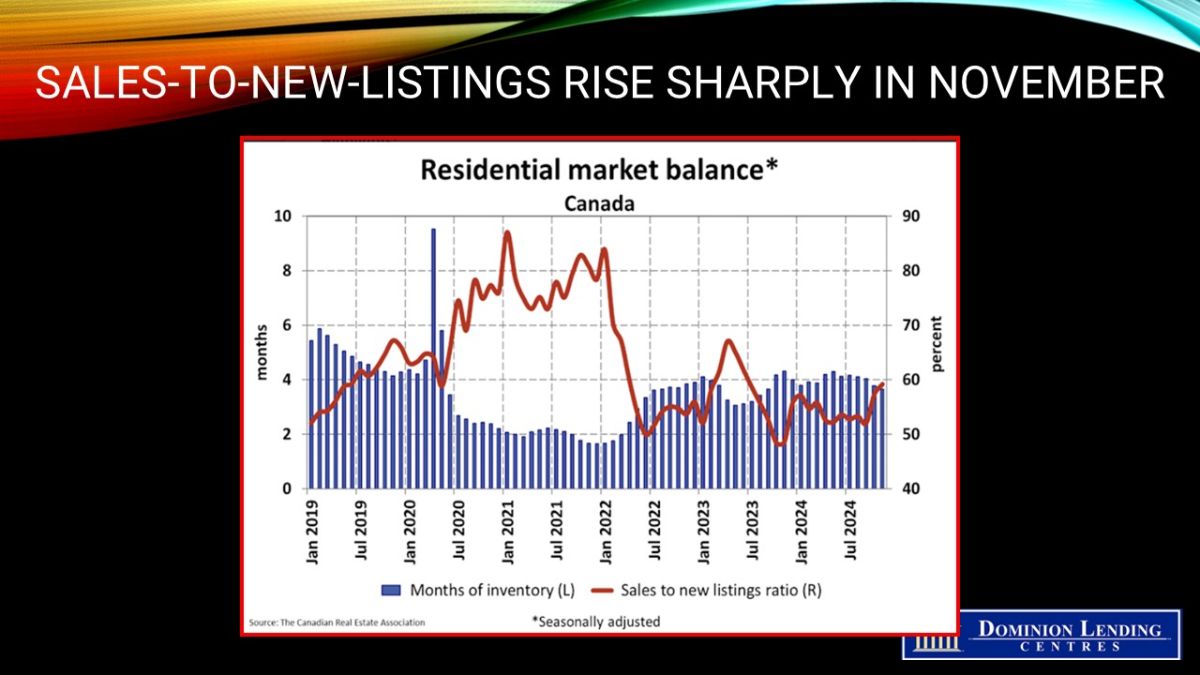

New Listings

New listings edged down 0.5% month-over-month in November, building on a larger 3% decline in October. With sales also rising in November, the national sales-to-new listings ratio tightened to 59.2%, up from 57.3% in October. Between April and September this year, the measure had been in the 52% to 53% range. The long-term average for the national sales-to-new listings ratio is 55%, with a sales-to-new listings ratio between 45% and 65%, generally consistent with balanced housing market conditions.

“October and November marked the start of the long-awaited rebound in resale housing activity, with the combination of lower borrowing costs and more properties to choose from coaxing buyers off the sidelines,” said James Mabey, CREA Chair.

A little more than 160,000 properties were listed for sale on all Canadian MLS® Systems at the end of November 2024, up 8.9% from a year earlier but still below the long-term average for that time of the year of around 178,000 listings.

There were 3.7 months of inventory nationally at the end of November 2024, down from 3.8 months at the end of October and the lowest level in 14 months. The long-term average is 5.1 months of inventory, with a seller’s market below about 3.6 months and a buyer’s market above 6.5 months.

{kind=link}

{kind=link}

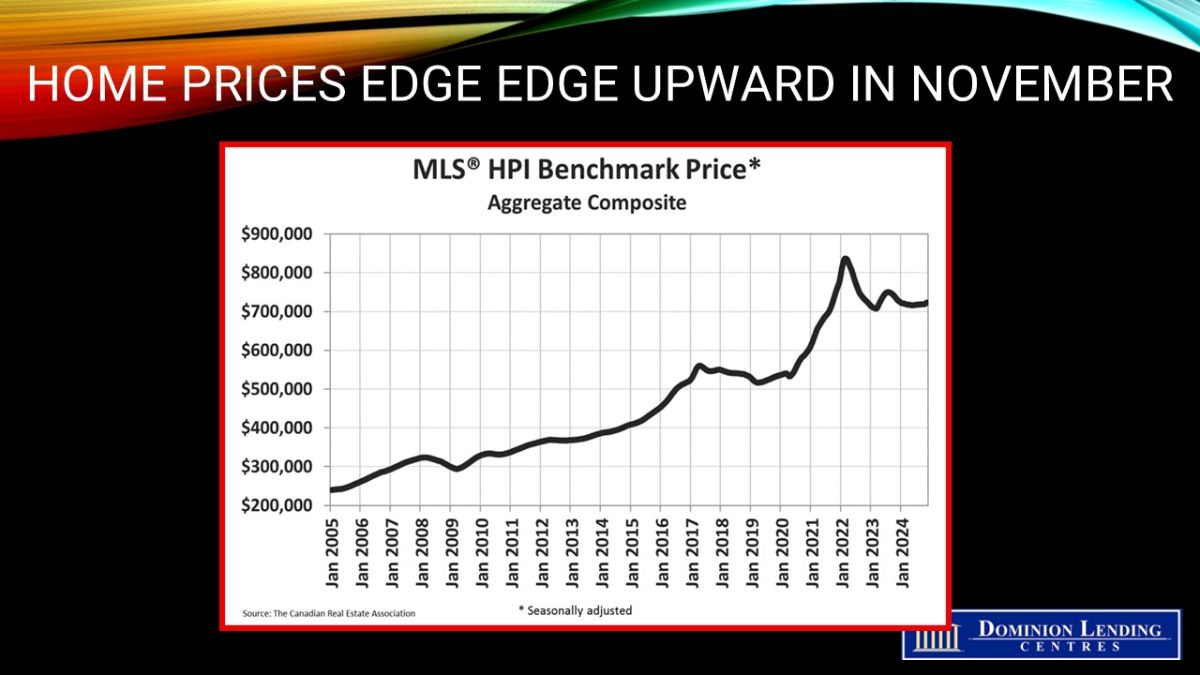

Home Prices

The non-seasonally adjusted National Composite MLS® HPI stood 1.2% below November 2023, the smallest decline since last April. The non-seasonally adjusted national average home price was $694,411 in November 2024, up 7.4% from November 2023.

{kind=link}

Bottom Line

The Bank of Canada’s aggressive rate-cutting and regulatory changes that make housing somewhat more affordable have provided kindling for the Canadian housing market. While the conflagration isn’t likely to peak until spring, a seasonally strong period for housing, activity has already started to pick up. The November uptick in home prices could provide more impetus for potential buyers to move off the sidelines. The new housing initiatives go into effect today and tomorrow.

Debt-to-income ratios for Canadian households have improved as growth in disposable incomes continues to outpace borrowing. This bodes well for more robust residential real estate activity as the Bank of Canada continues to cut rates, albeit at a slower pace. We expect quarter-point rate cuts until the overnight rate, now at 3.25%, falls to 2.5% or even lower if US tariffs are introduced.