Published by Sherry Cooper

Canadian Home Sales Dipped In July, New Listings Rose, And Prices Edged Up Modestly.

Housing Market Sales Dipped in July, Spooked By Rate Hikes

According to Shaun Cathcart, the Canadian Real Estate Association’s Senior Economist, “Following a brief surge of activity in April, housing markets have settled down in recent months, with price growth now also moderating with its usual slight lag. Sales and price growth are already showing signs of tapering off further in August in response to the Bank of Canada’s mid-July rate hike and messaging regarding above-target inflation for longer than previously expected. We’re probably looking at another round of back to the sidelines for some buyers until there’s a higher level of certainty around interest rates going forward.”

The good news is that the July inflation data, released today, will likely keep the Bank of Canada on the sidelines as core inflation has finally begun to slow. A host of economic indicators also point to Q2 GDP growth–released September 1–slowing to around 1% following the stronger-than-expected 3.1% growth in the first quarter. Labour market tightening eased in July with the decline in employment, rise in unemployment and continued downtrend in job vacancies. The central bank also welcomes the slowdown in the housing market.

Home sales recorded over Canadian MLS® Systems posted a small 0.7% decline between June and July 2023. Activity has been showing signs of stabilizing since May. While sales increased in July in more than half of all local markets, a decline in the Greater Toronto Area (GTA) tipped the national figure slightly negative. Sales were also down in the Fraser Valley, which, together with the GTA, offset gains in Montreal, Edmonton and Calgary.

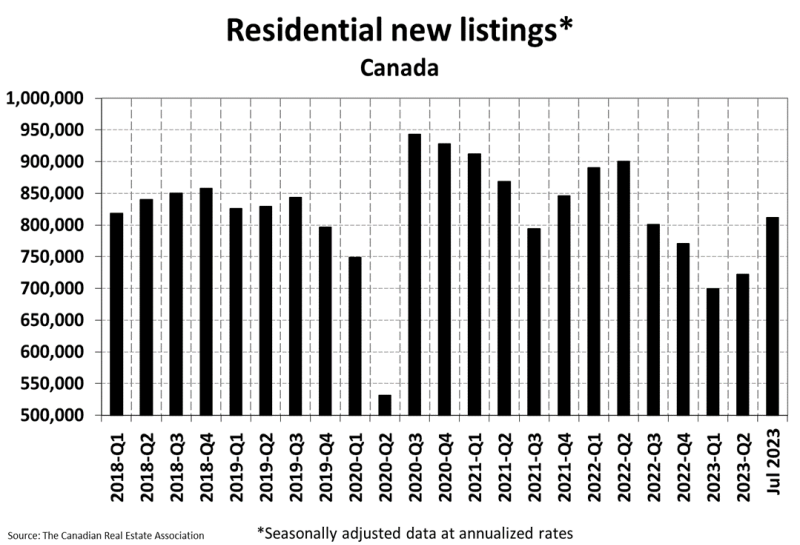

New Listings

The number of newly listed homes was up 5.6% monthly in July. Building on gains of 2.8% in April, 7.9% in May, and 5.9% in June, new listings have gone from a 20-year low in March to closer to (but still below) average levels by mid-summer.

With new listings outperforming sales in July, the sales-to-new listings ratio eased to 59.2% compared to 63% in June and a recent peak of 68% in April. That said, the measure remains above the long-term average of 55.2%.

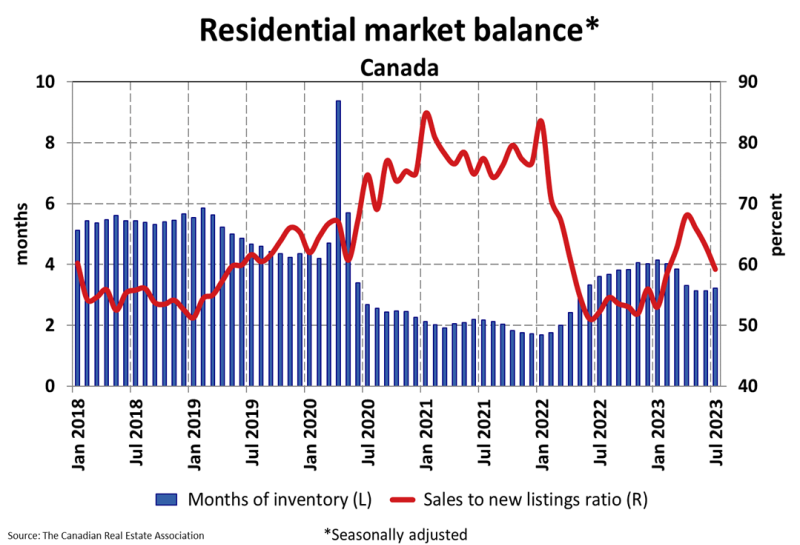

There were 3.2 months of inventory nationally at the end of July 2023, up slightly from 3.1 months in May and June.

While this was the first month-over-month increase since January, this measure is still a full month below where it was at the beginning of 2023 and almost two months below the long-term average for this measure (about five months).

{kind=link}

{kind=link}

Home Prices

The Aggregate Composite MLS® Home Price Index (HPI) climbed 1.1% month-over-month in July 2023—a larger-than-normal increase for a single month but only about half as large as the gains recorded in April, May, and June. This aligns with sales having levelled off as new listings have been recovering.

Despite the smaller gain at the national level, a monthly price increase between June and July was still observed in most local markets, as has been the case since April.

The Aggregate Composite MLS® HPI now sits just 1.5% below year-ago levels, the smallest decline since October 2022. Year-over-year comparisons will likely tip back into positive territory in the months ahead because prices continued to decline through the second half of 2022.

Bottom Line

With interest stabilizing, housing activity will gradually increase as more supply comes onto the market. The Bank of Canada will likely cut rates in 25 bps increments by June next year. Without a doubt, that will be good news for the housing market.

There remains huge excess demand for housing due to the rapid population growth. While the federal and provincial governments are working hard to increase the supply of affordable housing, the process is painfully slow and is unlikely to come close to the demand for homes for purchase or rent for the foreseeable future.