Published by Sherry Cooper

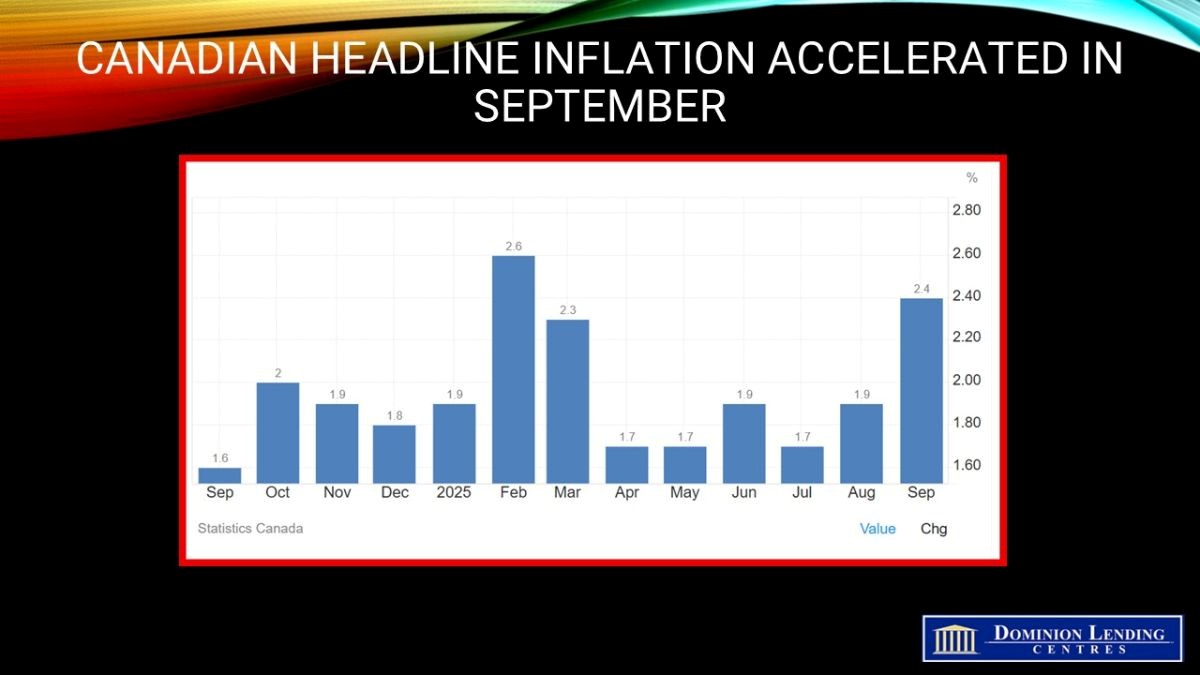

Canadian headline inflation slowed to 2.2% y/y in October, down from 2.4% in September..

Canadian Inflation Slows in October, But Not Enough to Trigger Another BoC Rate Cut in December

The Consumer Price Index (CPI) rose 2.2% on a year-over-year basis in October, down from 2.4% in September. The all-items CPI decelerated largely due to gasoline prices, which fell at a faster year-over-year pace in October (-9.4%) than in September (-4.1%). Excluding gasoline, the CPI rose 2.6% in October, matching the September increase. This was not enough of a decline to move the Bank of Canada off the sidelines, particularly given the recent strength in manufacturing sales, which surged 3.3% in September (estimated at 2.7%). Wholesale trade also surprised to the upside, 0.6% (estimated at 0.0%).

Slower growth in grocery prices further contributed to the CPI’s deceleration in October, which was moderated by surging cellular phone plan prices. Though grocery prices decelerated in October, prices remained elevated and have exceeded overall inflation for nine consecutive months.

Consumers paid more year over year in October for homeowners’ and mortgage insurance (+6.8%) and passenger vehicle insurance premiums (+7.3%). Among the provinces, prices rose the most in Alberta for both measures, with a 13.7% increase in homeowners’ home and mortgage insurance and a 17.8% increase in passenger vehicle insurance premiums.

Since October 2020, homeowners’ insurance and mortgage insurance prices have risen 38.9% nationally, while passenger vehicle insurance prices have risen 18.9%.

The index for property taxes and other special charges, priced annually in October, rose 5.6% year over year, down from 6.0% in 2024.

The CPI rose 0.2% month over month in October. On a seasonally adjusted monthly basis, the CPI was up 0.1%.

{kind=link}

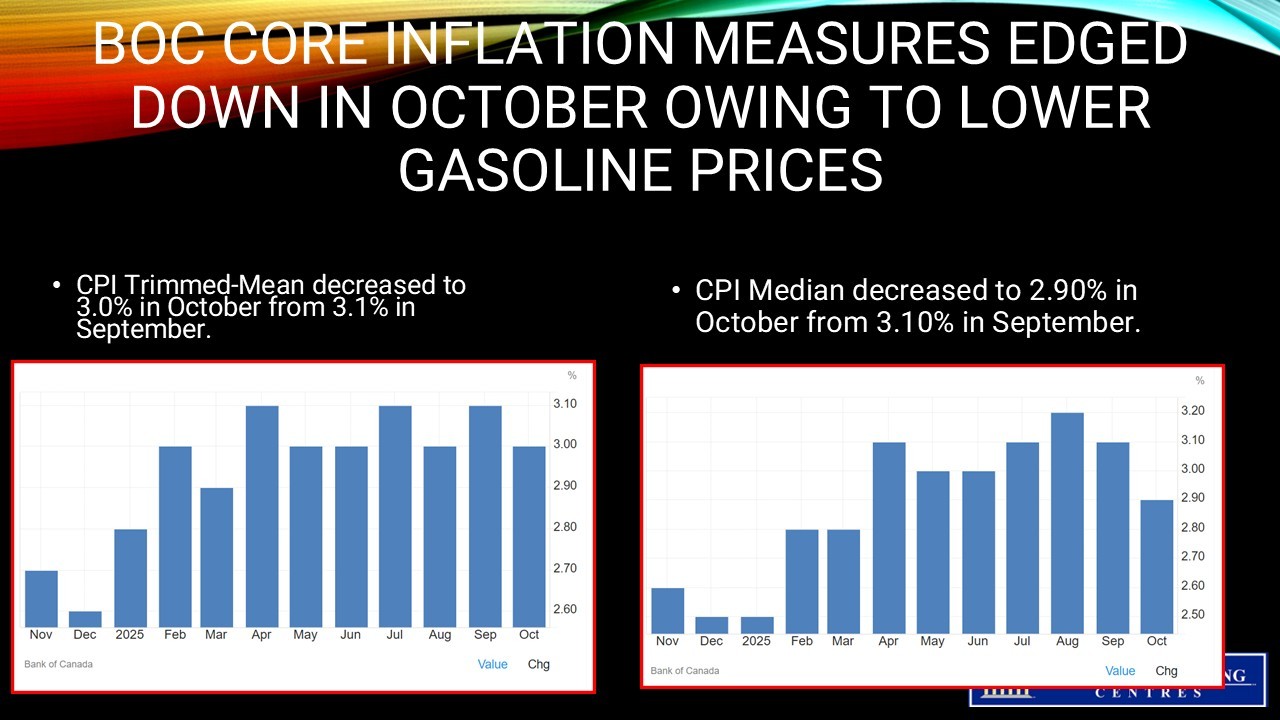

In October, both the CPI median and the CPI trimmed mean came in cooler than economists had expected. The average of these metrics was 2.95% in October.

The old measure of core—prices excluding food and energy—rose 0.3% m/m on an adjusted basis, boosting the yearly rate three full ticks to 2.7% y/y. A pop in cellular services was a significant driver there; in fact, the 7.9% y/y rise in all telephone services was the largest yearly increase since 1982. Still, a pullback in grocery prices, perhaps in part due to the rollback of retaliatory tariffs, helped moderate the Bank of Canada’s core measures. Median prices edged up just 0.1% m/m (s.a.), trimming the annual rate to 2.9%, while trim eased a tick to 3.0% y/y.

Rent perked up again to 5.2% y/y (from 4.8%), and remains the single most significant driver of inflation due to its heavy weight in the index.

{kind=link}

Bottom Line

This report does little to change the BoC’s view that underlying inflation remains close to 2-1/2%; but, if anything, most underlying metrics have been stuck a bit above that, or have just crept up there. In other words, this report is just another reason to believe the Bank is moving to the sidelines in December.