Published by Sherry Cooper

August Jobs Report Was Unexpectedly Weak.

Job Market Weakens As Economy Slows

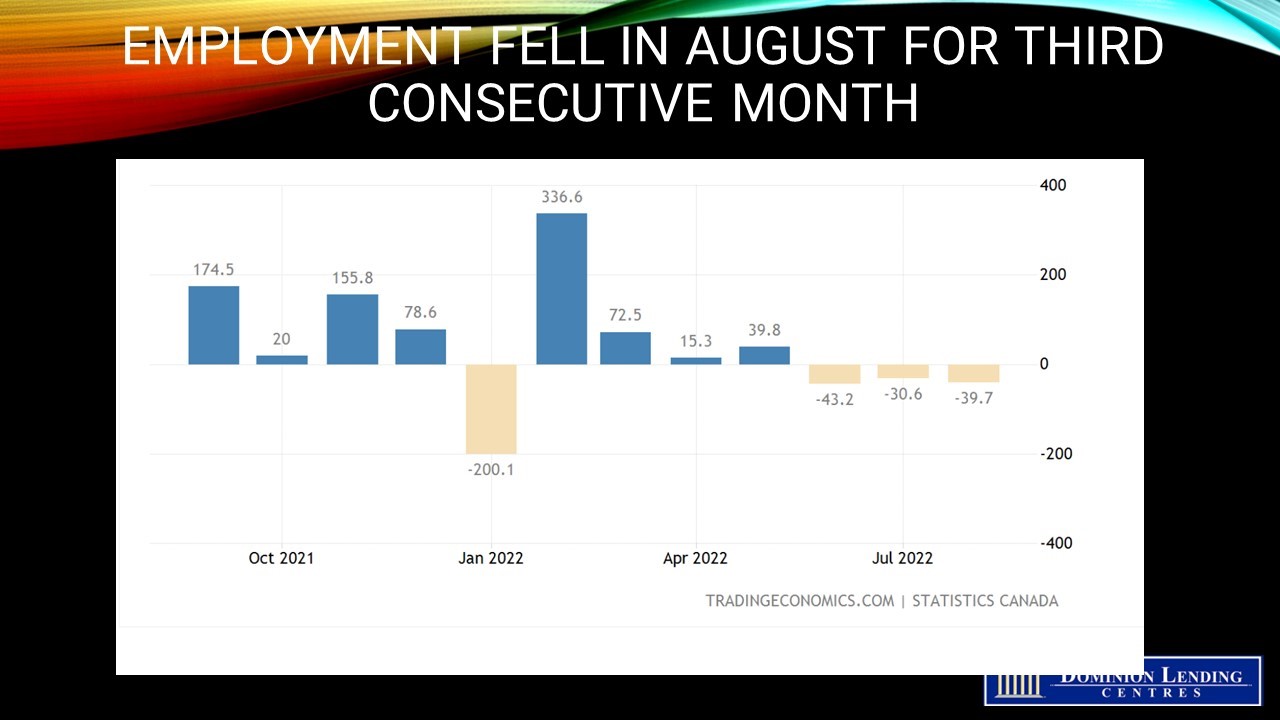

The August employment report, released this morning by Statistics Canada, was considerably weaker than expected. Higher interest rates have slowed the red-hot labour market. The Canadian economy shed 39,700 jobs in August, missing market expectations of a 15,000 rise and bringing cumulative declines since May 2022 to 113,500 (see chart below). The job losses were most significant in education and construction. Education employment in the summer months can be distorted by seasonal factors and changes in the start of the school year.

We know that residential construction projects have been postponed or cancelled owing to the rise in borrowing costs and the slowdown in home sales. There were also fewer workers in construction (-28,000; -1.8%) in August, with the decrease spread across several provinces, led by Alberta (-11,000; -4.6%) and Ontario (-10,000; -1.6%).Total employment fell in British Columbia, Manitoba, and Nova Scotia, while it increased in Quebec. There was little change in the other provinces.

Total hours worked were unchanged in August, following a decline in July (-0.5%). On a year-over-year basis, total hours worked were up 3.7%.

Hybrid Work Continues

Working from home continues to be an important feature of work for many Canadians, although the specific nature of the arrangement continues to shift. As of August, 16.8% of employed Canadians reported that they usually work exclusively from home, down from 18.0% in July and down 7.5 percentage points since the beginning of 2022. The proportion of workers with a hybrid work arrangement—those who usually work both at home and at locations other than home—increased by 0.7 percentage points to 8.6% in August.

{kind=link}

The Unemployment Surged From Record Low

The unemployment rate was 5.4% in August, up 0.5 percentage points from the record low of 4.9% observed in June and July. This was the first increase not coinciding with a tightening of public health restrictions since May 2020, when the unemployment rate reached its pandemic peak.

The unemployment rate increased for four of the six main demographic groups in August, including young men aged 15 to 24 (+1.2 percentage points, to 11.0%); women aged 55 and older (+0.7 percentage points, to 5.2%); core-aged men (+0.6 percentage points, to 4.6%); and core-aged women (+0.4 percentage points, to 4.5%). It was little changed among young women and older men.

The adjusted unemployment rate—which includes people who wanted a job but did not look for one—rose 0.5 percentage points to 7.3% in August. This increase was largely due to the rise in the number of unemployed rather than an increase in those who were outside the labour force but wanted work.

The hope is that the rising number of unemployed Canadians will help to fill the record job vacancies.

{kind=link}

Wage Inflation Accelerates To 5.4% in August

Particularly troubling for the Bank of Canada is the further acceleration in average hourly wages, which rose 5.4% on a year-over-year basis in August, compared with 5.2% in June and July (not seasonally adjusted).

Bottom Line

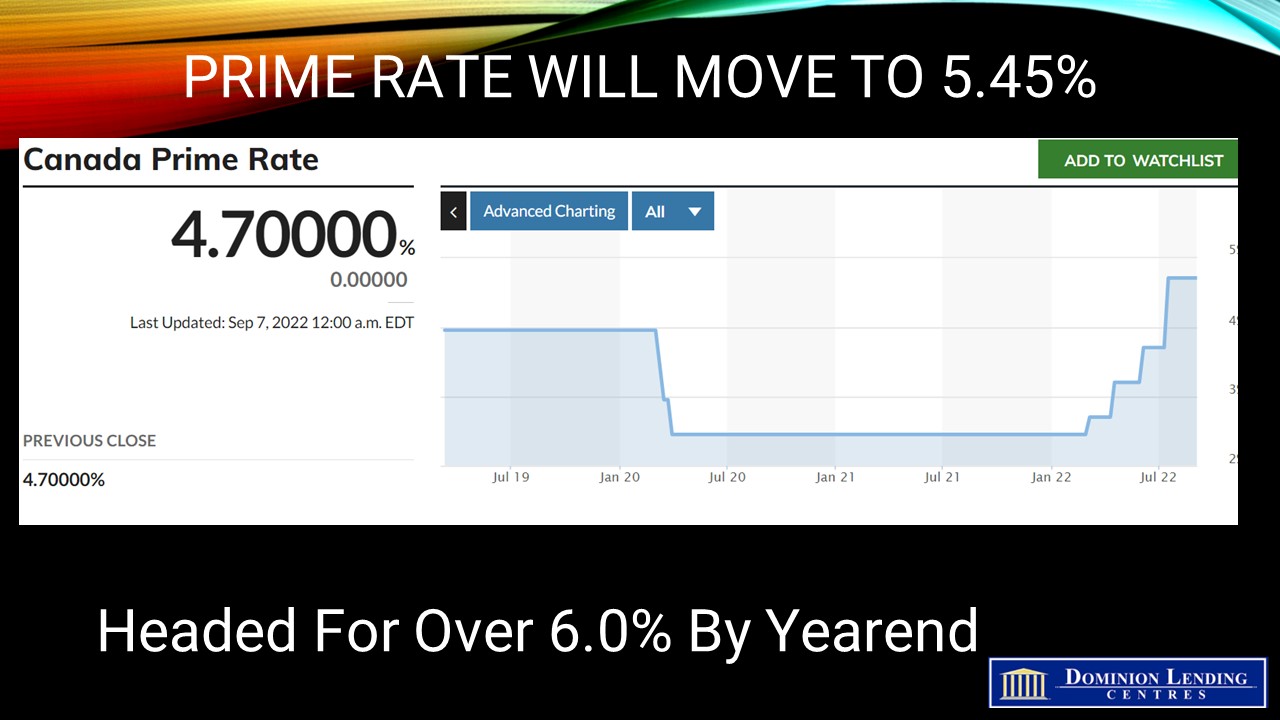

The Bank of Canada will welcome the cooling labour market, which will ultimately take the pressure off wage inflation. I don’t expect today’s weaker jobs report to change the Bank’s view that interest rates need to rise further in the coming months to return inflation to its 2% target level.

______________________________________________________________________________________________

In Other News Today, OSFI Refuses To Succumb to Pressure To Loosen B-20

Bloomberg News reported that despite the rise of mortgage rates heightening “the risk of a correction that could affect asset valuations and repayments” for Canadians, Peter Routledge, the Superintendent of Financial Institutions, said the Office of the Superintendent of Financial Institutions (OSFI) would not adjust the standards in B-20.

OSFI first created its Residential Mortgage Underwriting Practices and Procedures Guideline (B-20) in 2012. The guideline set expectations for residential mortgage underwriting for federally regulated lenders.

“The uncertainty and anxiety caused by a rising interest rate environment have, understandably, caused some Canadians to advocate for a loosening of the underwriting standards in Guideline B-20,” Routledge said.

“Let me reassure those of you who oppose a loosening of underwriting standards that OSFI will not do that.”

In June, Canada’s banking regulator announced that it tightened underwriting standards on combined loan plans such as reverse mortgages, mortgages with shared equity features and combined loan plans.

Routledge reiterated that OSFI is “constantly evaluating the MQR (Minimum Qualifying Rate) to measure its efficacy in sustaining sound residential mortgage underwriting.”

“Because Guideline B-20 touches home ownership, it gets an extraordinary amount of public attention – at least relative to all our other regulatory guidelines,” Routledge said.

“We accept this reality – housing is crucial to all Canadians, and Guideline B-20, whether we at OSFI like it or not, matters to Canadians. And so, our job is to address concerns with B-20 transparently and forthrightly.”